Venture capital (VC) is financial capital provided to early-stage, high-potential, high risk, growth startup companies. The venture capital fund makes money by owning equity in the companies it invests in, which usually have a novel technology or business model in high technology industries, such as biotechnology, IT and software. The typical venture capital investment occurs after the seed funding round as the first round of institutional capital to fund growth (also referred to as Series A round) in the interest of generating a return through an eventual realization event, such as an IPO or trade sale of the company. Venture capital is a subset of private equity. Therefore, all venture capital is private equity, but not all private equity is venture capital.

[1]

In addition to angel investing and other seed funding options, venture capital is attractive for new companies with limited operating history that are too small to raise capital in the public markets and have not reached the point where they are able to secure a bank loan or complete a debt offering. In exchange for the high risk that venture capitalists assume by investing in smaller and less mature companies, venture capitalists usually get significant control over company decisions, in addition to a significant portion of the company's ownership (and consequently value).

Venture capital is also associated with job creation (accounting for 2% of US GDP),

[2] the knowledge economy, and used as a proxy measure of innovation within an economic sector or geography. Every year, there are nearly 2 million businesses created in the USA, and 600–800 get venture capital funding. According to the National Venture Capital Association, 11% of private sector jobs come from venture backed companies and venture backed revenue accounts for 21% of US GDP.

[3]

It is also a way in which public and private sectors can construct an institution that systematically creates networks for the new firms and industries, so that they can progress. This institution helps in identifying and combining pieces of companies, like finance, technical expertise, know-hows of marketing and business models. Once integrated, these enterprises succeed by becoming nodes in the search networks for designing and building products in their domain.

[4]

History

A venture may be defined as a project prospective converted into a process with an adequate assumed risk and investment. With few exceptions, private equity in the first half of the 20th century was the domain of wealthy individuals and families. The Wallenbergs, Vanderbilts, Whitneys, Rockefellers, and Warburgs were notable investors in private companies in the first half of the century. In 1938, Laurance S. Rockefeller helped finance the creation of both Eastern Air Lines and Douglas Aircraft, and the Rockefeller family had vast holdings in a variety of companies. Eric M. Warburg founded E.M. Warburg & Co. in 1938, which would ultimately become Warburg Pincus, with investments in both leveraged buyouts and venture capital. The Wallenberg family started Investor AB in 1916 in Sweden and were early investors in several Swedish companies such as ABB, Atlas Copco, Ericsson, etc. in the first half of the 20th century.

Origins of modern private equity

Before World War II, money orders (originally known as "development capital") were primarily the domain of wealthy individuals and families. It was not until after World War II that what is considered today to be true private equity investments began to emerge marked by the founding of the first two venture capital firms in 1946: American Research and Development Corporation (ARDC) and J.H. Whitney & Company.

[5][6]

ARDC was founded by Georges Doriot, the "father of venture capitalism"

[7] (former dean of Harvard Business School and founder of INSEAD), with Ralph Flanders and Karl Compton (former president of MIT), to encourage private sector investments in businesses run by soldiers who were returning from World War II. ARDC's significance was primarily that it was the first institutional private equity investment firm that raised capital from sources other than wealthy families although it had several notable investment successes as well.

[8] ARDC is credited with the first trick when its 1957 investment of $70,000 in Digital Equipment Corporation (DEC) would be valued at over $355 million after the company's initial public offering in 1968 (representing a return of over 1200 times on its investment and an annualized rate of return of 101%).

[9]

Former employees of ARDC went on and established several prominent venture capital firms including Greylock Partners (founded in 1965 by Charlie Waite and Bill Elfers) and Morgan, Holland Ventures, the predecessor of Flagship Ventures (founded in 1982 by James Morgan).

[10] ARDC continued investing until 1971 with the retirement of Doriot. In 1972, Doriot merged ARDC with Textron after having invested in over 150 companies.

J.H. Whitney & Company was founded by John Hay Whitney and his partner Benno Schmidt. Whitney had been investing since the 1930s, founding Pioneer Pictures in 1933 and acquiring a 15% interest in Technicolor Corporation with his cousin Cornelius Vanderbilt Whitney. By far Whitney's most famous investment was in Florida Foods Corporation. The company developed an innovative method for delivering nutrition to American soldiers, which later came to be known as Minute Maid orange juice and was sold to The Coca-Cola Company in 1960. J.H. Whitney & Company continues to make investments in leveraged buyout transactions and raised $750 million for its sixth institutional private equity fund in 2005.

Early venture capital and the growth of Silicon Valley

A highway exit for Sand Hill Road in Menlo Park, California, where many Bay Area venture capital firms are based

One of the first steps toward a professionally-managed venture capital industry was the passage of the Small Business Investment Act of 1958. The 1958 Act officially allowed the U.S. Small Business Administration (SBA) to license private "Small Business Investment Companies" (SBICs) to help the financing and management of the small entrepreneurial businesses in the United States.

[11]

During the 1960s and 1970s, venture capital firms focused their investment activity primarily on starting and expanding companies. More often than not, these companies were exploiting breakthroughs in electronic, medical, or data-processing technology. As a result, venture capital came to be almost synonymous with technology finance. An early West Coast venture capital company was Draper and Johnson Investment Company, formed in 1962

[12] by William Henry Draper III and Franklin P. Johnson, Jr. In 1965, Sutter Hill Ventures acquired the portfolio of Draper and Johnson as a founding action. Bill Draper and Paul Wythes were the founders, and Pitch Johnson formed Asset Management Company at that time.

It is commonly noted that the first venture-backed startup is Fairchild Semiconductor (which produced the first commercially practical integrated circuit), funded in 1959 by what would later become Venrock Associates.

[13] Venrock was founded in 1969 by Laurance S. Rockefeller, the fourth of John D. Rockefeller's six children as a way to allow other Rockefeller children to develop exposure to venture capital investments.

It was also in the 1960s that the common form of private equity fund, still in use today, emerged. Private equity firms organized limited partnerships to hold investments in which the investment professionals served as general partner and the investors, who were passive limited partners, put up the capital. The compensation structure, still in use today, also emerged with limited partners paying an annual management fee of 1.0–2.5% and a carried interest typically representing up to 20% of the profits of the partnership.

The growth of the venture capital industry was fueled by the emergence of the independent investment firms on Sand Hill Road, beginning with Kleiner, Perkins, Caufield & Byers and Sequoia Capital in 1972. Located in Menlo Park, CA, Kleiner Perkins, Sequoia and later venture capital firms would have access to the many semiconductor companies based in the Santa Clara Valley as well as early computer firms using their devices and programming and service companies.

[14]

Throughout the 1970s, a group of private equity firms, focused primarily on venture capital investments, would be founded that would become the model for later leveraged buyout and venture capital investment firms. In 1973, with the number of new venture capital firms increasing, leading venture capitalists formed the National Venture Capital Association (NVCA). The NVCA was to serve as the industry trade group for the venture capital industry.

[15] Venture capital firms suffered a temporary downturn in 1974, when the stock market crashed and investors were naturally wary of this new kind of investment fund.

It was not until 1978 that venture capital experienced its first major fundraising year, as the industry raised approximately $750 million. With the passage of the Employee Retirement Income Security Act (ERISA) in 1974, corporate pension funds were prohibited from holding certain risky investments including many investments in privately held companies. In 1978, the US Labor Department relaxed certain of the ERISA restrictions, under the "prudent man rule,"

[16] thus allowing corporate pension funds to invest in the asset class and providing a major source of capital available to venture capitalists.

1980s

The public successes of the venture capital industry in the 1970s and early 1980s (e.g., Digital Equipment Corporation, Apple Inc., Genentech) gave rise to a major proliferation of venture capital investment firms. From just a few dozen firms at the start of the decade, there were over 650 firms by the end of the 1980s, each searching for the next major "home run". The number of firms multiplied, and the capital managed by these firms increased from $3 billion to $31 billion over the course of the decade.

[17]

The growth of the industry was hampered by sharply declining returns, and certain venture firms began posting losses for the first time. In addition to the increased competition among firms, several other factors impacted returns. The market for initial public offerings cooled in the mid-1980s before collapsing after the stock market crash in 1987 and foreign corporations, particularly from Japan and Korea, flooded early stage companies with capital.

[17]

In response to the changing conditions, corporations that had sponsored in-house venture investment arms, including General Electric and Paine Webber either sold off or closed these venture capital units. Additionally, venture capital units within Chemical Bank and Continental Illinois National Bank, among others, began shifting their focus from funding early stage companies toward investments in more mature companies. Even industry founders J.H. Whitney & Company and Warburg Pincus began to transition toward leveraged buyouts and growth capital investments.

[17][18][19]

Venture capital boom and the Internet Bubble

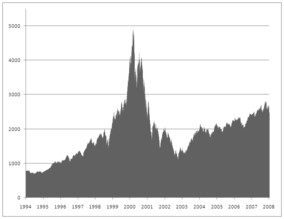

By the end of the 1980s, venture capital returns were relatively low, particularly in comparison with their emerging leveraged buyout cousins, due in part to the competition for hot startups, excess supply of IPOs and the inexperience of many venture capital fund managers. Growth in the venture capital industry remained limited throughout the 1980s and the first half of the 1990s, increasing from $3 billion in 1983 to just over $4 billion more than a decade later in 1994.

After a shakeout of venture capital managers, the more successful firms retrenched, focusing increasingly on improving operations at their portfolio companies rather than continuously making new investments. Results would begin to turn very attractive, successful and would ultimately generate the venture capital boom of the 1990s. Yale School of Management Professor Andrew Metrick refers to these first 15 years of the modern venture capital industry beginning in 1980 as the "pre-boom period" in anticipation of the boom that would begin in 1995 and last through the bursting of the Internet bubble in 2000.

[20]

The late 1990s were a boom time for venture capital, as firms on Sand Hill Road in Menlo Park and Silicon Valley benefited from a huge surge of interest in the nascent Internet and other computer technologies. Initial public offerings of stock for technology and other growth companies were in abundance, and venture firms were reaping large returns.

Private equity crash

The technology-heavy NASDAQ Composite index peaked at 5,048 in March 2000 reflecting the high point of the dot-com bubble.

The Nasdaq crash and technology slump that started in March 2000 shook virtually the entire venture capital industry as valuations for startup technology companies collapsed. Over the next two years, many venture firms had been forced to write-off large proportions of their investments, and many funds were significantly "under water" (the values of the fund's investments were below the amount of capital invested). Venture capital investors sought to reduce size of commitments they had made to venture capital funds, and, in numerous instances, investors sought to unload existing commitments for cents on the dollar in the secondary market. By mid-2003, the venture capital industry had shriveled to about half its 2001 capacity. Nevertheless, PricewaterhouseCoopers's MoneyTree Survey

[21] shows that total venture capital investments held steady at 2003 levels through the second quarter of 2005.

Although the post-boom years represent just a small fraction of the peak levels of venture investment reached in 2000, they still represent an increase over the levels of investment from 1980 through 1995. As a percentage of GDP, venture investment was 0.058% in 1994, peaked at 1.087% (nearly 19 times the 1994 level) in 2000 and ranged from 0.164% to 0.182% in 2003 and 2004. The revival of an Internet-driven environment in 2004 through 2007 helped to revive the venture capital environment. However, as a percentage of the overall private equity market, venture capital has still not reached its mid-1990s level, let alone its peak in 2000.

Venture capital funds, which were responsible for much of the fundraising volume in 2000 (the height of the dot-com bubble), raised only $25.1 billion in 2006, a 2%-decline from 2005 and a significant decline from its peak.

[22]

Funding

Obtaining venture capital is substantially different from raising debt or a loan from a lender. Lenders have a legal right to interest on a loan and repayment of the capital, irrespective of the success or failure of a business. Venture capital is invested in exchange for an equity stake in the business. As a shareholder, the venture capitalist's return is dependent on the growth and profitability of the business. This return is generally earned when the venture capitalist "exits" by selling its shareholdings when the business is sold to another owner.

Venture capitalists are typically very selective in deciding what to invest in; as a rule of thumb, a fund may invest in one in four hundred opportunities presented to it,looking for the extremely rare, yet sought after, qualities, such as innovative technology, potential for rapid growth, a well-developed business model, and an impressive management team. Of these qualities, funds are most interested in ventures with exceptionally high growth potential, as only such opportunities are likely capable of providing the financial returns and successful exit event within the required timeframe (typically 3–7 years) that venture capitalists expect.

Because investments are illiquid and require the extended timeframe to harvest, venture capitalists are expected to carry out detailed due diligence prior to investment. Venture capitalists also are expected to nurture the companies in which they invest, in order to increase the likelihood of reaching an IPO stage when valuations are favourable. Venture capitalists typically assist at four stages in the company's development:

[23]

-

Idea generation;

-

Start-up;

-

Ramp up; and

-

Exit

Because there are no public exchanges listing their securities, private companies meet venture capital firms and other private equity investors in several ways, including warm referrals from the investors' trusted sources and other business contacts; investor conferences and symposia; and summits where companies pitch directly to investor groups in face-to-face meetings, including a variant known as "Speed Venturing", which is akin to speed-dating for capital, where the investor decides within 10 minutes whether he wants a follow-up meeting. In addition, there are some new private online networks that are emerging to provide additional opportunities to meet investors.

[24]

This need for high returns makes venture funding an expensive capital source for companies, and most suitable for businesses having large up-front capital requirements, which cannot be financed by cheaper alternatives such as debt. That is most commonly the case for intangible assets such as software, and other intellectual property, whose value is unproven. In turn, this explains why venture capital is most prevalent in the fast-growing technology and life sciences or biotechnology fields.

If a company does have the qualities venture capitalists seek including a solid business plan, a good management team, investment and passion from the founders, a good potential to exit the investment before the end of their funding cycle, and target minimum returns in excess of 40% per year, it will find it easier to raise venture capital.

Financing stages

There are typically six stages of venture round financing offered in Venture Capital, that roughly correspond to these stages of a company's development.

[25]

-

Seed funding: Low level financing needed to prove a new idea, often provided by angel investors. Crowd funding is also emerging as an option for seed funding.

-

Start-up: Early stage firms that need funding for expenses associated with marketing and product development

-

Growth (Series A round): Early sales and manufacturing funds

-

Second-Round: Working capital for early stage companies that are selling product, but not yet turning a profit

-

Expansion : Also called Mezzanine financing, this is expansion money for a newly profitable company

-

Exit of venture capitalist : Also called bridge financing, 4th round is intended to finance the "going public" process

Between the first round and the fourth round, venture-backed companies may also seek to take venture debt.

[26]

Firms and funds

Venture capitalists

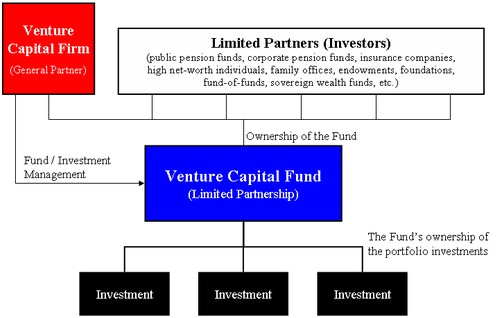

A venture capitalist is a person who makes venture investments, and these venture capitalists are expected to bring managerial and technical expertise as well as capital to their investments. A venture capital fund refers to a pooled investment vehicle (in the United States, often an LP or LLC) that primarily invests the financial capital of third-party investors in enterprises that are too risky for the standard capital markets or bank loans. These funds are typically managed by a venture capital firm, which often employs individuals with technology backgrounds (scientists, researchers), business training and/or deep industry experience.

A core skill within VC is the ability to identify novel technologies that have the potential to generate high commercial returns at an early stage. By definition, VCs also take a role in managing entrepreneurial companies at an early stage, thus adding skills as well as capital, thereby differentiating VC from buy-out private equity, which typically invest in companies with proven revenue, and thereby potentially realizing much higher rates of returns. Inherent in realizing abnormally high rates of returns is the risk of losing all of one's investment in a given startup company. As a consequence, most venture capital investments are done in a pool format, where several investors combine their investments into one large fund that invests in many different startup companies. By investing in the pool format, the investors are spreading out their risk to many different investments versus taking the chance of putting all of their money in one start up firm.

Diagram of the structure of a generic venture capital fund